Monthly Investment Note: June 2023

As we roll into the end of the first half of 2023, we continue to see inflation dominate the macroeconomic system, though with the main central banks taking time to consider their next steps in terms of rate increases.

The Euro (HICP) Inflation rate for May is 6.1% (and for Ireland is 6.3%) down from the 7% in April. Across the pond, inflation in the US is 4.9%, (May inflation date is available on 13.06.23) but with core inflation remaining stubborn, the rate at which inflation drops closer to the FED stated 2% inflation target will be slower and more difficult to achieve.

So, interest rate policies across the globe continue to focus on the Central Bank’s goals of inflation reduction with the US considering halting rates at 5.25% for this cycle (but might go another 0.25%) and the European Central Bank with rates at 3.25%, continued to signal that more rate rises were likely. Despite Saudi Arabia deciding to cut oil production by 1M bpd, Oil (Brent Crude) continues to trade below $80 pb ($76 pb at time of writing).

After weeks of negotiations and speculation in Washington, we finally saw a deal between the Republican & Democrat parties to raise the debt ceiling which provided some relief to the US & Global markets, but did anybody really think that the US would default on its sovereign debt obligations? Out of interest, US national Debt is currently ca. $31.8 Tn with a debt to GDP ratio of 96%, much higher than Ireland’s debt to GDP ratio which is ca. 60%.

Stocks in the Asia Pacific region also benefitted from news of a US debt ceiling agreement however, weaker than expected Chinese Purchasing Managers Index and a slower than expected post covid recovery in the region has seen muted returns in 2023. Indeed, China’s exports in May plunged 7.5% year over year to $283.5 billion, where Economists were only expecting a 0.4% drop. May’s fall was so steep that export volumes were lower than those at the start of the year, after accounting for seasonality and changes in prices signalling a slow and difficult recovery to growth.

Time will reveal how this plays out on the global markets in the coming months.

Global equities have continued their rally with the index of global stocks up 10.9% since the beginning of the year. While US equities have risen 11.5%, Japanese equities risen 12.9%, (mostly in the last month), it is now the European equities which underperform the global market with a rise of 10.7% this year so far; (all Euro hedged). This is a lesson for timing the Markets, and it is well known within investment circles that the biggest gains for the year occur over the period of less than 10 days. Timing the markets cannot be done consistently and better to stay within the markets when there is downward volatility, than dip in and out.

The strong performances of the US & Japanese markets are driven by the meteoric rise of the potential for Artificial Intelligence applications into virtually (no pun intended!) every facet of life. It seems that any company which can play a part in the “AI” story has seen phenomenal growth in its share price and this is in turn reflected in the fPE ratios of the NASDAQ which remain high at 24.8 times earnings compared to the overall S&P500 at 18.9 times earnings.

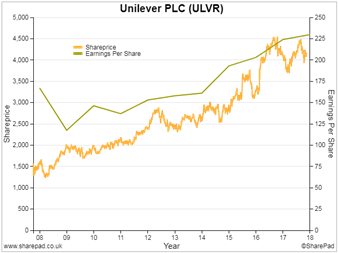

While the performance in European stocks is also impressive, it is driven (in large part) by the good value on offer with a plethora of companies showing strong balance sheets & free cashflows and trading at good value (fPE = 13 x) in other words good quality companies trading at good value and suitable for this economic cycle. A similar situation is seen in Japan with markets trading at 13.6 times forecast earnings and the UK at 14.2 times.